Should you be an aggressive investor?

Personal finance personalities tell you to take too much investment risk while society influences you to take too little, especially if you’re a woman. This article will help you determine how much risk to take.

Personal Finance Gurus Are Over-Simplifying Your Risk Tolerance

I’ve suggested before, presumptively, that many Madi Manages Money subscribers are aggressive investors.

The basis for my bold claim is rooted in demographics. Most of you reading this are like me; we’re women in our 30s with young children.

Decades will pass before you touch that money you’ve shoveled into your Roth IRA. So, from a purely clinical perspective, you can invest aggressively because your time horizon is long enough to recover from market dips.

But, we ignored important clues when making your preliminary ‘aggressive’ diagnosis. What about your emotions? How you feel while watching your account take a nosedive is part of the puzzle.

Turn a blind eye and run the risk of yeeting your stock portfolio into cash at a market bottom, like we saw a lot of first-time investors do during a bumpy 2022. 😔

Widely-accepted personal finance gospel preaches investing in low-cost index funds. With this I wholly agree, but it’s incomplete advice.

Invest in low-cost index funds of what? Implied in their superficial, blanket advice is that all young people should be investing in stock index funds only.

My experience has taught me differently. I’ve watched thousands of investors make detrimental decisions during market drops all because they’d assumed more risk than they were emotionally comfortable taking.

Your risk level is arguably *the* most important investment decision you’ll make. It’s directly linked to how much your money grows.

Women want and deserve to make a more thoughtful choice.

Define ‘Aggressive Investor’

An aggressive investor is someone who’s comfortable with her total portfolio in stocks.

Sure, more extreme tiers exist – like concentrating your money in cryptocurrency or microcap biotech stocks 😬 – but investing solely in a portfolio of equities punches your ticket into the club.

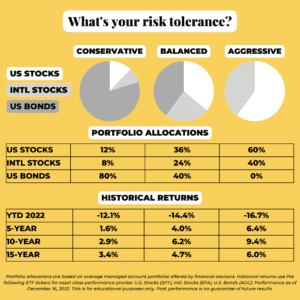

If you hired a financial advisor to manage your account as an aggressive investor, you’d usually get a portfolio that invests in 60% U.S. stocks and 40% international stocks.

Historically, here’s what the ride has looked like.

Being an aggressive investor has the obvious appeal of maximizing how much money you could make over time. Like all things in finance, this comes with a catch.

You’ll need to stomach greater volatility (i.e. ups and downs) and have a higher chance of losing money, especially if you’d scratch an itch to rotate into safer investments during a market drop.

Awareness of how you’ll react to this type of financial stress is a prerequisite to aggressive investing.

2022 made for a painfully perfect example. The aggressive example (above) will be down about -17% to finish this year. Zooming out, that same portfolio averaged a positive 6% annually over the past 15 years.

By comparison, the more conservative option had a lower upside of 3.4% per year, but the portfolio is down less in 2022 at -12%. (More conservative investments do still carry risk!)

These numbers explain why a long time horizon (of at least ten years) is a common thread among all wise aggressive investors.

Historically, that’s been long enough to recover from market drops. Any shorter and you run a higher probability of losing money.

Related: Anxious About the Stock Market?

Internalized Sexism Stymies Women Investors (Especially Aggressive Ones)

A 2021 Fidelity survey asked 2,400 retirement plan participants – half men and half women – whether or not they were investors.

Surprisingly, only 33% of the women responded with a yes. 🤔

This is despite already knowing that 100% of them were investing in their 401(k)s. They didn’t think of themselves as investors.

Taking this one step further, women who do view themselves as investors are less likely than men to consider themselves aggressive ones.

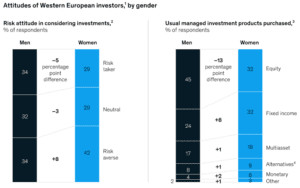

A McKinsey study that surveyed 2,300 women and 2,700 men in Europe found only 29% of the women considered themselves risk takers compared to 34% of men.

When it came to how opposite sexes invested their money, this effect stretched even further. Only 32% of the average woman’s portfolio was invested in equity, compared to 45% of a man’s.

This is heartbreaking. A 13% discrepancy in portfolio exposure creates big swings in the amount of money each gender earns.

Collectively, women will underperform men measurably over a lifetime.

The bias on display here runs deep. From an early age, young men are praised for taking risks, especially ones that lead to profit.

Young women, on the other hand, are taught that ambition and our desire to earn money is seen as unattractive and undesirable.

Women have learned that labeling ourselves as ambitious or assertive carries real professional and social penalties. Author and journalist, Stephanie O’Connell, aptly coined the term “ambition penalty” to describe this phenomenon.

It partly explains why women feel uncomfortable being labeled as aggressive. To our detriment, this bias subconsciously influences our investment choices, unless we force it into the light.

Nothing’s wrong with wanting or earning more money. If you have a long time horizon and the moxie to ride out some bumpy markets, let it rip. Aggressive investing isn’t just for the boys.

Can I Handle Being an Aggressive Investor?

You’ll need two things:

- A high ability to take risk.

- A high willingness to assume risk.

Your ability to take risk is the more objective part. Based on the underpinnings of your family’s financial situation, what type of uncertainty can you withstand?

The amount of time until you plan to use a specific chunk of money is the most important factor. If your time horizon is at least ten years long, historical probabilities say you can afford to dial up your risk.

Your willingness is all about how you feel. How you’ll react to market fluctuations is willingness.

You should consider your ability & willingness in tandem to determine what type of investor you are. Your goal is to strike a balance between maximizing your returns without feeling like you’re white-knuckling a rollercoaster.

An example is the clearest way to explain. Enter Megan. 🦸♀️

Megan is a 30-year old investor in her 401(k) at work. Her family is financially secure, with her and her partner’s jobs paying the bills and then some. She isn’t planning on touching her 401(k) money for at least another 30 years.

Her ability to take risk in this account is pretty darn high.

But, when Megan imagines her $100,000 401(k) dropping by -17%, she feels anxiety swell in her chest. She can even picture herself staring at her screen, sweating, with her cursor hovered over the ‘SELL’ button.

Her willingness to take risk is lower.

Given Megan’s lengthy time horizon, she should still peg her starting point on the aggressive side. From there, she could take the edge off by introducing conservative holdings, perhaps landing closer to an 80% stock and 20% bond portfolio.

When in doubt, know that you’re better off saddling up a portfolio you’re comfortable riding through up and down markets than trying to time ins and outs.

Oscillating between an aggressive portfolio and a more conservative one is a recipe for failure.

Related: Risk Tolerance – How to Handle Willingness & Ability Mismatch

Summary

The online personal finance community is telling you to take too much risk. Society is telling you to take too little. What’s a girl to do?

When in doubt, look to your timeline for direction. If you can leave your money invested for ten years or more, you can take some risks.

From there, dial up or down your exposure to conservative investments, like bonds, until you meet a portfolio that you can consistently cozy up to.

Don’t discount the amount of risk that you’re capable of taking. I’m confident that the more educated you are on personal finance and investing, the more comfortable you’ll be taking risks.

Gaining knowledge builds fortitude and realistic expectations.

My personal opinion? If you can gentle-parent through a knock-down, drag-out toddler meltdown over a Baby Shark Vacuum in Target, you’re going to be just fine handling market volatility. 😉

Women are aggressive investors, too.

Resources:

- Fidelity: Women & Investing Study 2021

- McKinsey & Company: Wake Up & See the Women

- Stephanie O’Connell’s Website

A note on the hypothetical model portfolios shown in this article. Determine what’s right for you based on your timeline (ability) and how comfortable you feel taking risk (willingness), not based on past performance you’d like to replicate. The purpose of these portfolios is to demonstrate the relative difference between them, not to provide exact performance figures.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investments may be appropriate for you, consult with your financial advisor.