This post weighs the pros and cons of selling vs. renting out your primary residence. Specifically, we’ll look at how this decision impacts eligibility for the IRC Section 121 exclusion, a major tax break for homeowners.

My husband and I are approaching our breaking point. Our 1,100 square foot, 3 bed, 2 bath (including a Pittsburgh potty), is feeling a little snug. With a daughter, two work-from-home jobs, and virtually no closets, we could use a little more space. We’re in the early stages of looking for a new home and *potentially* converting our primary residence to a rental property.

An actual photo of the clearance in our primary bathroom.

As we’re learning, the question of Should I sell or rent my house? isn’t as simple as meets the eye. We own a home with a low cost basis, which is code for “you shoulda seen this thing when we bought it,” but it also means we’ll want to think about capital gains taxes when we sell.

We purchased our place for $55,000 in 2018 and have put about $30,000 of work into it. Today, our property is worth at least $160,000, according to Lord Zillow. Assuming we can sell it for that much and would pay about $10,000 transaction costs, I’d estimate our capital gain at ~$65,000.

($160,000 – ($55,000 + $30,000 + $10,000) = $65,000)

Thanks to the IRC Section 121 exclusion, an extremely generous piece of the U.S. tax code for homeowners, my husband and I qualify to exclude all of this capital gain from our taxable income, as long as we play by the IRS’ rules. At a 15% capital gains tax rate, this would bring our tax savings to ~$10,000. Not a bad incentive to cash out!

Despite the tax savings dangling before me – and how much I’d love to plow the sale proceeds into my investment accounts – we’re still toying with the idea of converting our primary residence to a rental property when we move, at least for a period of time. We own our home outright and have a low-interest-rate mortgage on the house next door, which could make for convenient (in theory🥴), side-by-side rentals.

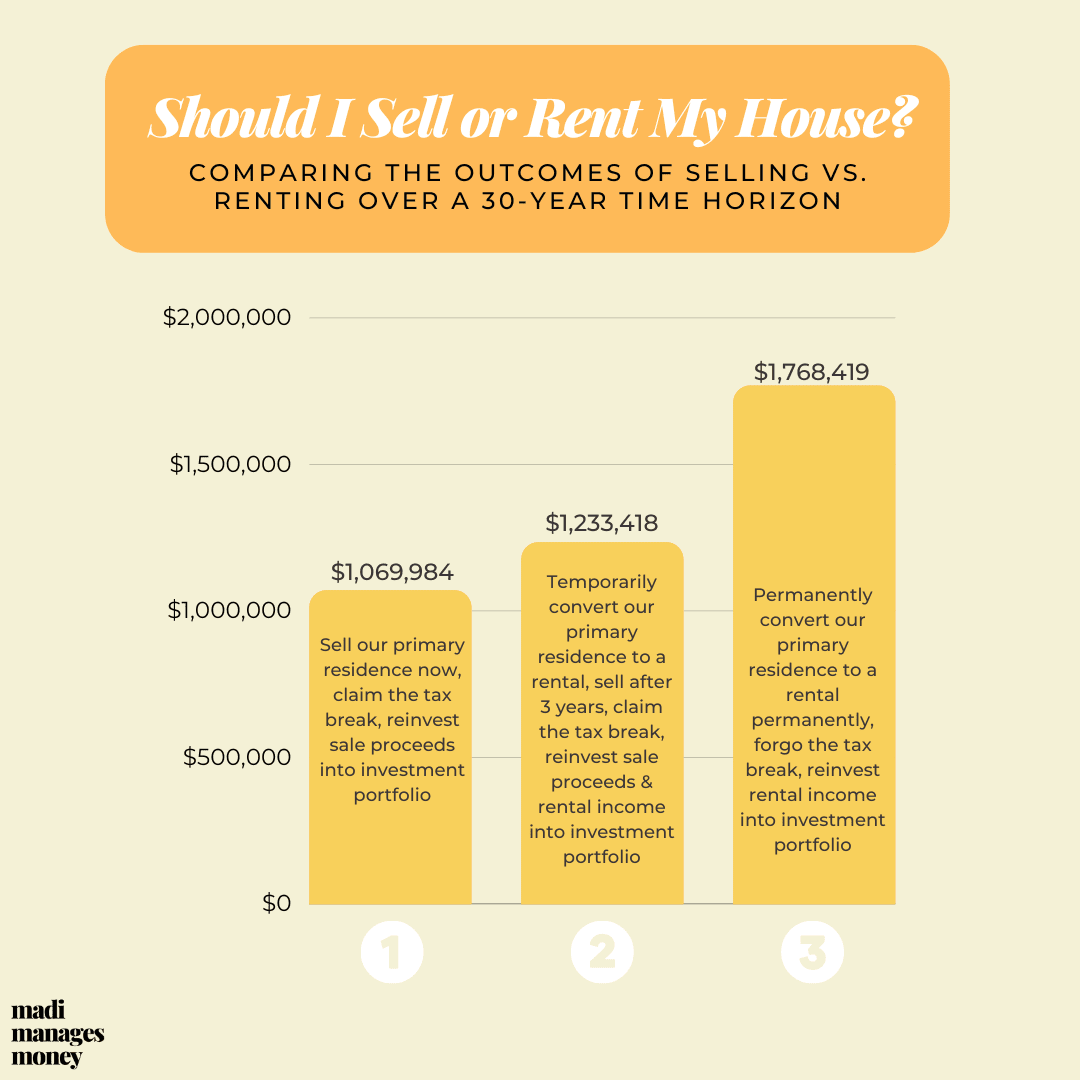

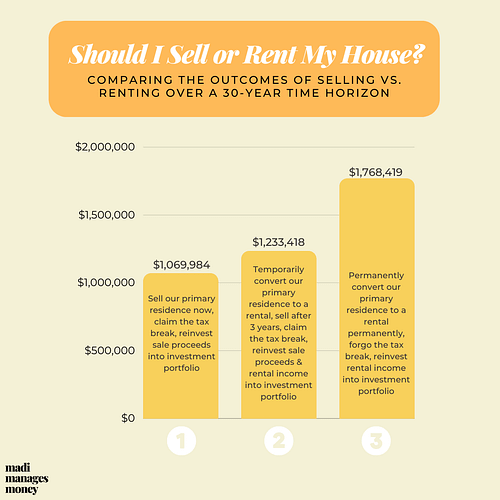

This leaves me with three possible scenarios to compare to determine if I should sell or rent my house.

- Sell our primary residence now, claim IRC Section 121 tax savings, reinvest sale proceeds into our investment portfolio for the long term

- Temporarily convert our primary residence to a rental, sell after 3 years, claim IRC Section 121 tax savings, reinvest sale proceeds & rental income into our investment portfolio

- Permanently convert our primary residence to a rental for 30 years, forgo Section 121 tax savings, reinvest rental income into our investment portfolio

My preference before doing this analysis is option 2. I’d like to test out the rental waters for 3 years. After that, we’d sell to take advantage of the IRC Section 121 capital gain exclusion unless we really ❤️ the landlord game. My mind could be changed, however, if my projections tell me something different.

But first, what is the IRC Section 121 exclusion?

Up to $250,000 in capital gains for individuals, or up to $500,000 in capital gains if you’re married, filing jointly, can be excluded from taxes when you sell your primary residence under IRC Section 121. Any gains in excess of these amounts are subject to capital gains tax.

To qualify for the full $500,000, both spouses must live in the home for at least 2 of the 5 years before you sell your property. It’s okay if the home is owned by just one spouse, however – still counts! You can claim this exemption as frequently as every two years.

Occupying the house, or meeting the “use” test, is where things can get tricky, because there are a lot of ways to live in a house 2 out of the last 5 years. To prevent real estate investors from coming up with creative ways to take advantage of the exclusion, the IRS created something called non-qualified use. At its most basic level, having too much non-qualified use can reduce or altogether eliminate your IRC Section 121 eligibility.

Because what counts as non-qualified use can get complicated, I’ve asked a tax professional to weigh in. Grant Dougherty of Dougherty Tax Solutions simplified it for us.

“Non-qualified use of the home is basically any time the residence was not used as a primary residence. Mostly, this is going to be using the property as a rental. It does not include temporary absence due to health reasons or being deployed.”

The good news is if you’re a homeowner who has lived in your primary residence for at least 2 years and then decided to rent it out until you hit the 5-year window, you’re in the clear from non-qualified use. This is thanks to a special clause in the tax code. (Oh, you know, IRC Section 121(b)(5)(C)(ii).)

This clause frees homeowners from having to count the 3-year period after they move out until they sell (even if they convert their primary residence to a rental) as non-qualified use. In essence, it preserves full access to the Section 121 exemption if you’d like to try your hand at renting before you’d sell. BUT! You’re still beholden to the 2 of 5 years timeline.

Should I sell or rent my house? The analysis.

Knowing I have tax savings from IRC Section 121 in my back pocket, this leaves me with three scenarios to compare. I could sell now, sell after a little bit, or hold on and rent the property for the long term.

I used the following assumptions & values in my analysis to determine if I should sell or rent my house. My assumed timeline is 30 years.

- Annually, my investment portfolio will grow at 7%, and real estate values & rental income will grow at 2.5%.

- I’ll fall in the 24% marginal income tax bracket and 15% capital gains tax bracket. I assume the tax code will be similar in 30 years.

- I assume I can sell my home for $160,000 today, or I could rent it out for $1,400 a month.

- Real estate transaction costs are estimated at 6% of the sale price.

- I can maintain a 90% occupancy rate as a rental.

- I didn’t build any explicit property maintenance costs into these estimates. But, I also didn’t deduct expenses from my taxable rental income. In other words, I’m assuming the amount I’ve underestimated in upkeep costs is offset by the amount I’ve overestimated in taxes paid.

- I have no mortgage on this home.

I’m a numbers gal, and the selling vs. renting results still surprised me. Converting our primary residence to a rental for the long term turned out to be the most favorable option…by a convincing margin. This even entails forgoing the tax savings we’d get from the Section 121 exclusion entirely.

Why did the numbers shake out this way?

Before performing this analysis, I thought the tax break I’d get from qualifying for the Section 121 exclusion (~$10,000) was more important than it actually is. On top of that, I assumed putting a sizable lump sum into the market from the sale of our house (of about $150,000) would compound faster than piecemealing rental income into our investment portfolio over the years.

My hypothesis was wrong for a few reasons.

By keeping the property as a rental, I’m benefitting from three separate growth engines. I’d have an appreciating home, plus monthly rental income that feeds a compounding investment portfolio. According to the numbers, it’s worth it for me to forgo the tax benefit I’d get today (or in 3 years, if I rented temporarily) in order to maintain access to all three.

I’d also expect these numbers to look different if you live in a HCOL area and have a greater unrealized gain to manage. In the grand scheme of things, our $65,000 in appreciation actually isn’t huge. If you have closer to the $500,000 maximum of capital gains that can be excluded by a couple who is married, filing jointly, you could be looking at a tax savings of $75,000.

If your primary residence is highly appreciated, compare the tax savings you can expect from Section 121 to the monthly rental income you can garner. In our case, we’ll be able to earn back our lost tax savings after just over a year of renting our place. This is partly because we don’t have a mortgage on this property.

If you do have a mortgage, make sure you consider the net monthly cash flow you expect to earn from your rental, and not just gross rental income, into your analysis. According to the Dallas Fed, as of September 2022, just 31% of outstanding mortgages had a rate exceeding 4%. So, even if you do have a mortgage, I like the chances that you can make decent cash flow from your property.

Conclusion: Renting Wins

Should I sell or rent my house? The numbers say, convincingly, I should rent it. As it turns out, taking advantage of the homeowner’s exclusion is less of a no-brainer than you’d guess.

Consult a tax planner as you work through these mental gymnastics, especially if you have a highly appreciated property. Truth be told, part of the reason I’ve thought so deeply about this decision is because I’ve been burnt by IRC Section 121 before.

I owned a duplex from 2014 to 2020, renting out half and living in the other. When I sold the property at a sizable gain, I was surprised to learn not all of it was tax exempt. Because I rented half of my home, half of it fell under the non-qualified use definition for several years of my holding period.

I had to pay tax on the price appreciation (plus any depreciation I took) on the rented half of the duplex. It was a real bummer, because after paying taxes on the sale, I hardly broke even on my rental business. Much of this pain could have been avoided had I consulted an accountant upfront.

What’s right for you will depend on several factors. These include how much your home has appreciated, your mortgage rate, and what you can collect in rent vs. fetch for a sale price. Run your numbers, hire a pro, and don’t let the tax tail wag the investment dog like I nearly did!

Our plan is still to convert our primary residence to a rental upon moving out for at least 3 years. But now, based on this analysis, it’s looking like we’re in the rental game for the long haul. 🤠

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investments may be appropriate for you, consult with your financial advisor.