After reading this independent review of the Pennsylvania 529 Plan, you’ll know:

-

What makes the PA 529 Plan a great option for PA residents.

-

When to choose the PA 529 Guaranteed Savings Plan vs. Investment Plan.

-

How the PA 529 investment options work.

I’m a financial professional who has experience evaluating 529 plans and a mother who invests in the PA 529 Plan for my own daughter. Otherwise, I have no affiliation with this program.

Lightning Round Primer on 529 Plans ⚡️

529s are college savings accounts equipped with tax advantages to encourage you to save for college. Often, parents open them for their children, but anyone can open one, even for yourself.

Here are the 529 account tax benefits that you just can’t get with a regular old savings or investment account:

- State tax deductions for contributions (deduct up to $17,000 for individual filers or $34,000 for joint filers, assuming both spouses make at least $17,000)

- Tax-deferred investment growth (meaning that you don’t incur taxes on growth or dividends while money is in the account)

- Tax-free withdrawals (as long as the money’s used for qualified education expenses)

There are two broad types of 529 plans: guaranteed savings plans & investment plans. All fifty states sponsor at least one of these types.

A guaranteed savings plan enables you to prepay future college tuition at today’s rates. (A prepaid tuition plan is another name for them.) Generally, most of these plans have in-state residency requirements, as is the case with PA.

Investment plans, on the other hand, allow you to invest for future college expenses. They can usually be opened across state borders by any U.S. citizen age 18 and older. For that reason, we’ll compare to some investment plans outside of PA in this article.

Overall PA 529 Plan Review: Ideal Choice for PA Residents

The PA 529 Plan is a competitive offering for Pennsylvanians, providing perks that residents can’t get if they choose to invest elsewhere. As of November 2023, the PA 529 Investment Plan is just one of two states that has earned a Gold Medal rating by independent research firm, Morningstar.

Pennsylvania offers both a guaranteed savings plan and an investment plan. Per beneficiary, your account balance can reach a maximum of $511,758, one of the highest 529 asset caps in the country. And, you don’t have to pick one or the other; a guaranteed account and an investment account can be opened for the same beneficiary.

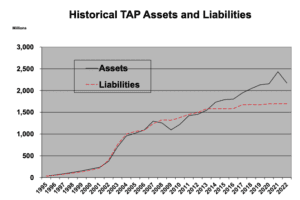

Remarkably, PA is just one of nine states to offer a guaranteed plan. As of June 30, 2022, assets in this plan were well funded to meet future commitments to investors. If the guaranteed plan is right for you (more on how to determine that next), this funding status should give you confidence.

The investment plan uses industry leader, Vanguard, as manager of the plan. Vanguard brings to the table world-class index fund investing and helps keep investment expenses low for the hoi polloi, like you and me.

Investment choices in the plan are broad enough to meet your needs yet still succinct enough to not feel overwhelming. You can choose to create a customized portfolio yourself or outsource managing investments entirely by selecting a prepackaged portfolio.

To support my overall assessment, Pennsylvania’s investment plan is just one of two states to earn a Gold Medal rating from Morningstar, an established research firm that’s an authority in 529 plan analysis. Morningstar reviews state 529 investment plans on an annual basis, covering over 90% of all 529 plan assets. Utah is the only other state to earn a Gold Medal rating.

Pennsylvania offers these perks to residents on assets invested in its 529 plan.

- Exemption from PA Inheritance Tax

- Protection from PA creditors

- Exclusion when determining PA state financial aid eligibility

There is a convenient exception to the list above. PA residents can still claim a state income tax deduction for contributions to any 529 plan – not just Pennsylvania’s.

There has been a motion to eliminate this benefit, however, that if passed, would only increase the attractiveness of the PA 529 Plan to residents.

Finally, money from either type of account can be used for a wide range of identical qualified education expenses. These include tuition at most colleges, universities, community colleges, grad schools, and technical schools in the U.S. and abroad – not just in Pennsylvania.

You can also use up to $10,000 per year at private or religious K-12 schools. Plus, room and board, required books, qualified education loans, and equipment and covered, among other expenses.

Related Post: The 529 to Roth IRA Rollover (What Parents Should Know)

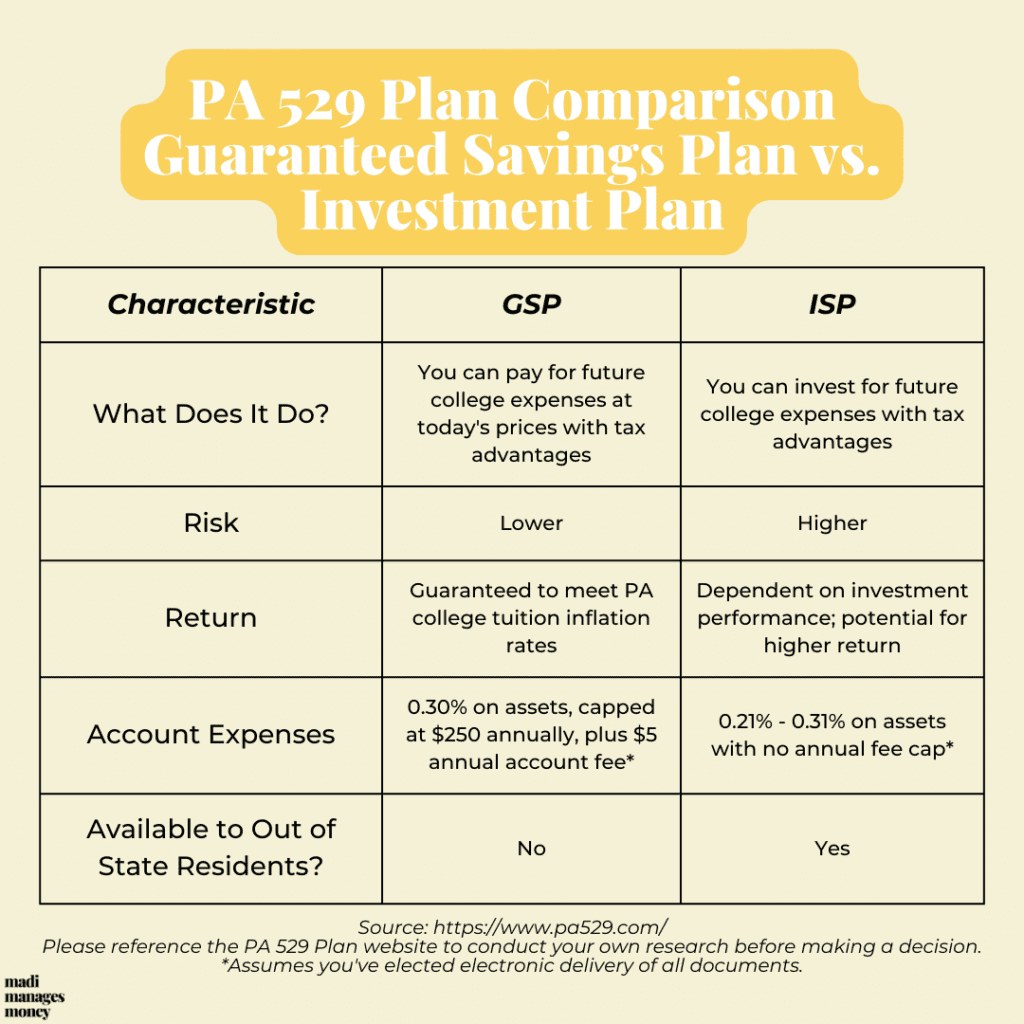

PA 529 Guaranteed Savings Plan vs. Investment Plan

Next, we’ll compare details of the two types of college savings programs that Pennsylvania offers.

- PA 529 Guaranteed Savings Plan (GSP)

- PA 529 Investment Plan (ISP)

So, which PA 529 Plan is better? The answer to that question will depend on your comfort level with investment risk and the timeline until your beneficiary heads to college. Here’s what you need to know to decide.

The PA 529 Guaranteed Savings Plan

This is your lower-risk option. It guarantees you the ability to pay for future college expenses at today’s prices.

When you contribute money to a PA 529 GSP account, the money goes into a special investment fund established by the Commonwealth of PA. Regardless of how this investment fund performs, the growth that your account earns is always the college tuition inflation rate.

That’s precisely why it’s your lower-risk option – because the state’s investment fund, not you, is on the hook for covering tuition increases.

(If you’re familiar with how a pension works, the PA 529 GSP functions much like that. A company pension fund assumes the risk of paying out a guaranteed future stream of income to you.)

And, it’s worth noting that the state appears prepared to make good on these obligations. The annual actuarial report of that special investment fund shows that the plan is adequately funded. Its assets out weigh its liabilities (i.e. future commitments to investors).

No one has a crystal ball, but based on what we know today, this should give you some confidence in choosing the PA 529 GSP as your college savings plan.

Now, back to this all-powerful tuition inflation rate that your account will be credited each year. How is it determined?

Every year, Pennsylvania calculates averages of the actual tuition increases experienced by in-state schools. These averages are grouped by type of school. It’s this rate that you earn.

To ballpark expected annual tuition increases, below are the projected rates and groupings from the PA 529 GSP website.

- Private Four-Year Colleges: 5.25%

- Ivy League Colleges: 5.25%

- State-Related University Average: 4.50%

- Community Colleges: 4.00%

- State System of Higher Education: 3.75%

(Note: these are the state’s estimates. For exact credit rates, reference the PA 529 Plan website.)

When you open a PA 529 GSP account, you’ll be asked to make your best guess at which type of school the beneficiary might attend. This helps you estimate how much to save.

If you select the Private Four-Year College option because it has the highest growth rate, and then your child decides to attend a community college, it doesn’t mean your money will stretch further or grow more. Instead, the plan will retroactively apply the tuition rate of the type of school the beneficiary actually attends.

On the flip side, if you expected Junior to attend community college, but then he stuns you with an acceptance letter to an Ivy League school, you’re covered.

Considering that you’ve made it this far into a blog post about 529 plans, I have you squarely pegged as someone who covers their bases. 🙂 In a nutshell, there’s no way to game the system, but simultaneously, you don’t need to stress about picking the wrong type of school, either.

Now, let’s cut over to how the guaranteed plan compares to the investment plan. If you’re swooning over the PA 529 GSP, with its inflation protection and guarantees, let’s address the elephant in the room.

Since the return of the guaranteed plan is, well, guaranteed, you’ve mitigated your risk of earning less than the college tuition inflation rate, but you’ve also eliminated your chances of earning more than it.

It’s probable that over long periods of time (like if you’re starting a 529 account for your baby), there’s a real opportunity cost to consider. The guaranteed plan could produce less than the investment plan. And, the lower return that you earn on a 529 account, the more you end up forking over for college.

Read More: Is the PA 529 Guaranteed Savings Plan Right for My Family?

The PA 529 Investment Plan

Meet your higher-risk option. It’s an investment account used to save for college, and like with any investment, returns are not guaranteed. Generally, these accounts will be invested in a mixture of stocks and bonds at a risk tolerance selected by you.

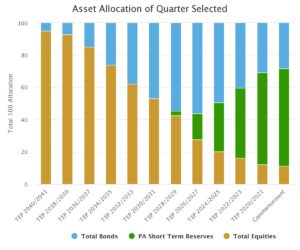

The PA 529 ISP has a versatile menu of investment options managed by Vanguard. You can pick from two subsets of investments: 11 Target Enrollment Portfolios or 14 Individual Enrollment Portfolios.

Target Enrollment Portfolios (Do it for me.)

Target Enrollment Portfolios simplify investing for college. You select one portfolio based on the year the beneficiary is anticipated to enroll, and the investment manager does the rest. (If you’re familiar with what Target Date Funds are, perhaps from a 401(k) plan, these work just like that.)

PA 529 Plan Target Enrollment Portfolio allocations as of 10/31/2022

At first, your Target Enrollment Portfolio will hold mostly riskier investments, like stocks. Doing so early on gives your portfolio a better chance at earning higher returns while still allowing enough time to recover from a down stock market.

As your beneficiary gets closer to college time, that same Target Enrollment Portfolio automatically begins to swap out some stock holdings in favor of more conservative ones, like bonds. To be precise, Pennsylvania makes these adjustments to de-risk your portfolio every two years. That means no buying or selling required on your part!

Come time to use the money, a final conservative allocation is reached. Holding relatively more stable investments during that time reduces the chances that you’d need to withdraw from your 529 portfolio after a negative fluctuation.

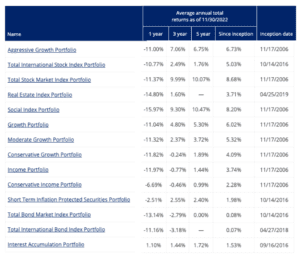

Individual Enrollment Portfolios (I’ll do it myself.)

The Individual Enrollment Portfolios are static investment options that follow a consistent mandate. The Aggressive Growth Portfolio will be invested aggressively, the Conservative Income Portfolio will be invested conservatively, and so on.

As of the end of November 2022, here are the PA 529 ISP investment options and their historical returns.

As you can see, the plan offers enough choices to build a fully diversified portfolio, but the menu isn’t overwhelming. You’re able to pick up to five investments to customize your account. (Any more would be diversification overkill.💀)

I don’t pick investments based on which ones have the highest historical return (or lowest, for that matter). ‘Past performance does not predict future results’ isn’t just a disclaimer – it’s the truth!

I show this to you, instead, to give you a realistic idea of the types of ups and downs you must be willing to accept if you take on investment risk with the PA 529 ISP. While all of the Since Inception returns are positive, you can see that many investments are down meaningfully over the past one to three years.

Personally, because I’m comfortable taking investment risk and my daughter is only one year old, I invest her account wholly in the Aggressive Growth Portfolio. On the surface, it appears to be just one investment, but if you peek under the hood, it’s a fully-diversified portfolio holding thousands of domestic and international stocks.

Eventually, I’ll de-risk the account to provide some stability before the years that we’ll make withdrawals. When I do that, and to what degree, will largely depend on our financial situation in about ten years from now. Until then, we sit tight and let time do its thing. ⏰

Related Post: Invest for Retirement or My Kid’s College Tuition? How to Do Both.

PA 529 Plan Expense Comparison

Asset-based fees for the PA 529 GSP are 0.40%, with a $500 annual cap. This fee is reduced to 0.30%, capped at $250 annually, for accounts that elect electronic delivery of documents. Plus, all guaranteed savings plan accounts are subject to a minimum fee of $5 annually.

(For perspective on the GSP fee caps, you’d need $84,000 to $125,000 in your account to hit them.)

All-in, asset-based fees for the PA 529 ISP range from 0.21% to 0.31% with no fee caps. These totals are made up of 0.19% in program management fees, plus 0.02% to 0.12% in expenses on the underlying investments. The investment plan charges a $10 account maintenance fee that can be waived if you elect electronic delivery of all documents.

To put this to scale, a 0.30% fee on a $10,000 investment would equal $30 per year. Then, tack on the minimum account fees of $5 to $10 to arrive at your total expected annual cost of $35 to $40.

When using this information to make a decision, remember that guaranteed savings plans generally have a state residency requirement. So, if that’s the right choice for you, prepare to get cozy with the Commonwealth! There’s little sense comparing to other states’ prepaid plans because they aren’t available to you.

Expense information is relevant if you’re going the investment plan route. Compared to other states, the PA 529 ISP charges competitive fees, but it’s not the absolute cheapest option.

For instance, by opening an investment account with either Michigan or Utah (the only two states with a higher rating by Morningstar), you could expect annual fees as low as $11 to $15 on a $10,000 account.

Consider, though, that for the ~$20 in annual savings that you could achieve (per $10,000 invested) with an out-of-state plan, you’d be forgoing the benefits available to you with the PA 529 Plan as a Pennsylvanian.

For any assets in your PA 529 Plan, these perks include exemption from PA Inheritance Tax, protection from PA creditors, and exclusion when determining state financial aid eligibility. For me, that savings isn’t worth going out of state, but perhaps I’d consider it if I had a much larger account.

Here’s a link to a 529 plan fee study tool for anyone who wants to conduct further research on fees by state.

The Bottom Line:

- Both types of PA 529 Plans are solid choices that offer special benefits to Pennsylvanians. As a PA resident, I haven’t found another 529 plan that’s compelling enough to go out of state.

- Choose what type of 529 plan is right for your family based on your comfort with investment risk & the amount of time until the beneficiary uses the money.

- If you’re not comfortable with investment risk or you have a short time until the beneficiary needs the money, the PA 529 Guaranteed Savings Plan might be right for you. This plan enables you to pay for future college costs at today’s rates.

- If you’re comfortable with investment risk and you have a young beneficiary, take a hard look at the PA 529 Investment Plan.

Related Post: Overfunded 529 Plan? These Are Tax-Efficient Solutions.

Resources:

The tuition inflation figures used in this post are from the Pennsylvania 529 Plan website. They’re based on historical and projected rates of tuition inflation at each type of institution, but there can be no assurance that they will accurately reflect future increases. Historical performance, credit rates, and other figures used in this article are for educational purposes only. Consult the Pennsylvania 529 Plan website for exact figures before making a decision.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investments may be appropriate for you, consult with your financial advisor.