I’m a fee-only financial planner who works with parents of young children. Here are some financial mistakes I see parents regularly make that fly under the radar.

- Saving your baby’s money in a savings account.

- Not having enough life insurance coverage.

- Investing for your kids before you’re on track for your own retirement.

Common. Preventable. Easily corrected. Here are some of the top financial mistakes made by parents.👇

Saving your baby’s money in a savings account

Storing cash from birthdays in savings accounts for kids is a relic from boomer parenting. Back then, a savings account (or maybe CDs if they were feeling spicy) was their best option to store money until you bought your first car or graduated from college. They didn’t have frictionless access to online investing like we do.

Today, it’s virtually free to invest online. We can make long-term investments on behalf of our kids when they’re young, which maximizes the amount of time their money grows.

Investing with an extremely long time horizon – especially when you buy and hold – is nothing short of magic.🦄

Now, you might be wondering, How bad could a savings account be? Well, worse than you’d think.

Let’s pretend your baby receives a total of $1,000 for their first birthday. (Rich Aunties and Grandma showed up with fat stacks.) You plan to give this money to your child in 17 years when they turn 18.

If you kept the money in a savings account, and inflation was about 3% per year (which is in line with long-term historical averages), your child’s $1,000 would be worth more like $596 when they reach 18.

Yes, $1,000 will still be sitting in their account, but you’re guaranteeing a loss of $404 in purchasing power. Money becomes less valuable over time.

Now, what if you invested the birthday money instead?

If you invested the $1,000 in a low-cost stock market index fund for the next 17 years, you could end with an estimated $3,159. This assumes you were able to earn a 7% annual return.

That’s a +$2,563 difference with little to no extra work on your part. In fact, your job is to invest the money and then do nothing!

Don’t touch it for 17 years, aside from adding more if you’d like. (This part makes investing easier than using CDs or shopping around for savings account yields. You’ll need to refresh CDs every time they reach maturity.)

Generally, the only reason someone should hold cash in a checking account is for emergency savings or for spending within the next two-ish years. Babies don’t have too many immediate needs that the Bank of Mom isn’t covering. 💰

Related Post: It’s Too Early to Open a Bank Account for Your Kids (but Not for the Reason You think)

Inadequate life insurance coverage

When I dig into the life insurance coverage many parents have, especially those of young children, I often discover they’re underinsured. Underinsured means the payout you’d receive should you pass away isn’t enough to cover your family’s financial needs.

(This payout is affectionally dubbed as the “death benefit” by the life insurance industry.)

Being underinsured seems to happen for two primary reasons. The first is simply that we don’t know how much coverage we actually need. The second has to do with purchasing the wrong type of policy.

Let’s start with understanding the amount of coverage you’d need.

At a minimum, I recommend adding together the following future expenses to form your estimate.

- Estimated annual living expenses for each year your kids are financially dependent on you

- Cost of college tuition (if you want to cover some of it for your kids)

- Liability balances (especially your mortgage)

The idea is to ensure your spouse could comfortably afford your family’s life if you weren’t there. As such, you’d be taking out two policies (one for each spouse) for this total.

Both parents should have policies on their life, even if one is a breadwinner and one works in the home. If one spouse earns more, perhaps you’d want to make their policy larger. As for the spouse who works in the home, they should still have life insurance coverage, even if it’s not quite as large as the earner.

Here’s the reality. If the non-earning spouse passes away, the breadwinner will have more to do than simply hire a nanny to fill their shoes. It’s realistic to assume a breadwinner may downshift their own career to take a more active role running the home if the spouse who absorbs more invisible labor isn’t there.

Related Post: I’m a CFP & a Mom | Here’s My Life Insurance Coverage

Families with young children also often have the wrong type of life insurance coverage.

Sometimes, families rely on group term life insurance as a primary means of coverage, or they have expensive whole life insurance policies. The steep cost of whole life insurance premiums makes accessing the death benefit you need cost-prohibitive.

Group term life insurance is usually offered through and subsidized by your employer. It pays a death benefit equal to a multiple of your salary (usually between 1-3x) for as long as you work for that company. Once you’re no longer an employee, say sayonara to this coverage.

Group term insurance is a great start and a way to supplement third-party coverage, but it’s usually not enough if you have kids. As a guide, a best practice is to estimate the amount of coverage your family needs at roughly 10-12x your annual earnings. (This is a great data point to compare to the analysis we did above!)

10-12x your earnings is likely more than you can get through group term life, unless your company has a juicy supplemental policy.

Further, by relying on your group term insurance through work, you’re forgoing the opportunity lock in low, fixed premiums on term insurance.

By shopping for term life insurance policies when you’re in your 20s and 30s, you can lock in lower monthly premiums than you could when you’re in your 40s and 50s.

Let’s say you’re 40 and have two kids under five. You stay at your current company for the next ten years, until you reach 50. When you resign, you lose access to your group term policies, and your new employer has pretty meh life insurance benefits.

You still need coverage for the next 15 years, until your kids are financially independent. So, you find yourself on the hunt for term life insurance quotes at age 50 and realize how much cheaper this would’ve been if you put the policy in place sooner.

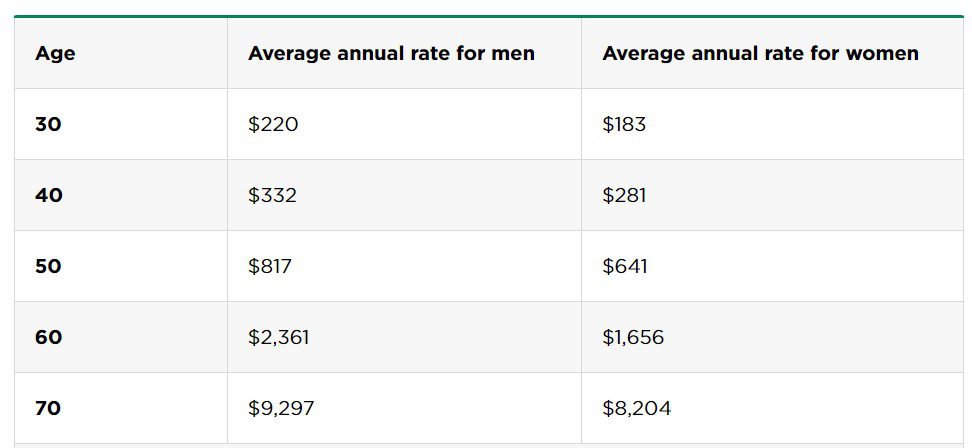

Here’s a comparison of annual term insurance premiums you can expect based on your age. These are for a $500,000 death benefit over a 20-year term. The source is Nerdwallet.

The recommendation is this: Take maximum advantage of any group term life insurance policies offered to you at work, especially if they’re subsidized by your employer.

Additionally, I’d consider shopping for term life insurance outside of your employer. You can lock in lower premiums at a younger age. This policy will stay in place regardless of your employment status, so you don’t have to re-shop insurance if you job hop.

Whole life insurance is another place where families are led astray, sometimes by salesmen. These policies come with steep monthly premiums that can be 15x (or much more!) than that of a term insurance policy with an equal death benefit.

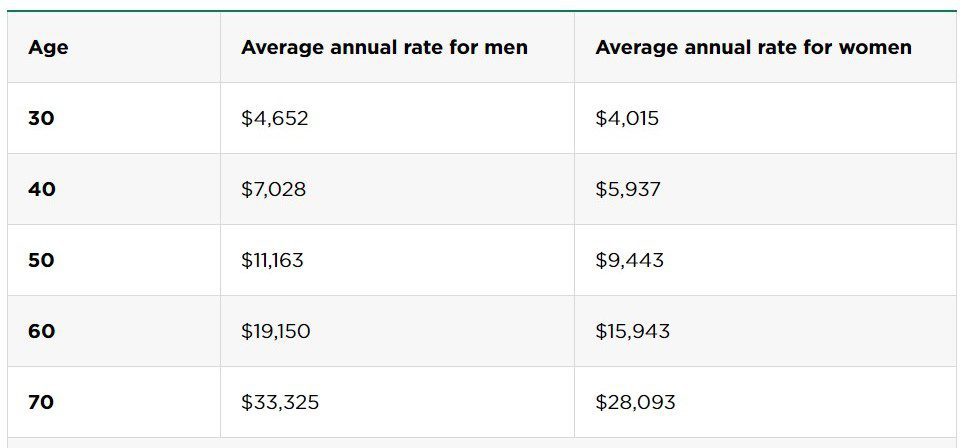

Here are December 2023 industry estimates for whole life insurance policies with a $500,000 death benefit. The source is Nerdwallet.

Whole life insurance is designed to stay in place for your entire life. Thus, the insurer expects you to fork over higher premiums because it’s probable they’ll eventually pay your death benefit.

🚩 Higher monthly premiums are an initial red flag, but here’s where insurance salesmen place their hooks into parents. They position whole life insurance as a way to store value in your insurance policy, even if you end up never using it. With this type of policy, a piece of each premium you pay gets stored in something called “cash value.”

Cash value is a lousy investment, if you want to call it an investment at all. It keeps pace with inflation, at best.

For most young families with competing financial priorities (childcare🙈, college🙉, mortgage🙊), term life insurance will be the move. Term insurance allows you to maximize the death benefit your family receives for a low monthly premium. Then, if you have extra monthly cashflow, it’s better off invested for the long term than collecting dust in the cash value of a whole life policy.

What parents don’t like about term insurance is that it’s a pure expense that hopefully you’ll never use. No part of the (much lower) monthly premium is stored anywhere, making it a bit like “renting” access to your death payout.

Whole life insurance is only appropriate in certain circumstances, like if your family is absolutely caked up or if you have a lifelong dependent.

(“Absolutely caked up” is a technical term that means you’re maxing out all of your tax-advantaged accounts, year after year, and have a cushy arsenal of assets in a taxable brokerage account. You’re on the hunt for another place to store assets on a tax-deferred basis. Whole life insurance can be used for this.)

Investing for kids before your own retirement

This financial mistake parents make is a tough one. Parents with the absolute best of intentions want to save and invest for their kids, sometimes even before they save for themselves.

I’ve heard things like, “I’m a lost cause, so why wouldn’t I just focus resources on my kids?”

I get it, but investing for kids before you’re on track for your own retirement is short-sighted. I’d double down to even say it’s selfish.

Why the harsh words? Because I don’t think the future will play out quite like parents hope.

As you age, retirement is the only financial goal you can’t borrow to cover. Think about it. Buying a home? Mortgage. New car? Auto loan. Wanna go to college? Student loans.

However, there aren’t lenders lining up at the opportunity to bankroll your living expenses from 65 to 95, only for you to die and not pay them back.

Plus, we’re going to live longer and have more expensive retirements than any other generation before us, especially women. The life expectancy of a 35-year old woman in the US is about four years longer than a man.

Even if you invest for your kids with no strings attached, your children aren’t robots. When you’re struggling in retirement as your children find success as adults, they’ll feel obligated to help you, no matter what you tell them.

You’re setting them up to be another sandwich generation instead of gifting them the privilege to worry about their own families.

How do I know if I’m on track? Here are some barebones numbers to consider.

My husband and I are 33 & 34 years old. The good old Social Security Actuarial Tables say my life expectancy is about 82 years old. Assuming we retire at 65, that leaves us with 17 years of retirement to afford.

If we want to spend about $70,000 a year in today’s dollars during each of those years, we’ll need at least $1.5 million saved by the time we enter retirement in ~31 years.

There are two ways we could get to our $1.5 million, assuming we can earn a 7% return.

- We could invest at least ~$14,000 a year until 65.

- We could invest a lump sum of ~$185,000 today.

This means we would need to have at least $185,000 invested for retirement already TODAY, or we’re able to consistently invest ~$14,000 every year for the next three decades to afford the absolute bare minimum in retirement.

In this estimate, I’m assuming our taxes in retirement essentially net out with Social Security income. I’m also assuming we die deadass broke according to schedule, in our early 80s.

If your family’s expenses look anything like ours (or are higher), and you don’t already have at least $185,000 saved or are able to consistently invest $14,000 per year, it’s premature to start regularly contributing to college savings accounts or other investment accounts for your kids.

Related Post: Invest for Retirement of My Kid’s College Tuition? How to Do Both.

Preventable & easily correctible

Financial mistakes parents make are committed with the best of intentions. Maybe we’re replicating what our parents did for us, #tiktokmadeyoudoit, or you took a cue from that coworker who seems to have her financial sh*t together.

Whatever your inspiration, you’re doing your best. No one is born with innate financial literacy, even though it feels like we’re expected to have it.

I’ll end with great news. All of these missteps are preventable and easily correctable.

They’re as simple as changing an insurance policy, opening a brokerage account, or practicing some financial self care. Plus, I genuinely believe all of these choices have the potential to make your financial life substantially easier.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investments may be appropriate for you, consult with your financial advisor.