What life insurance coverage do parents need? I’m a mother and Certified Financial Planner. We’ll take an unfiltered look at my own policy as an example.

Everyone’s favorite subject! Our inevitable demise!

Life insurance fills the financial gap left in the wake of a breadwinner or primary caretaker’s passing. At its most basic level, life insurance requires you to make ongoing premium payments in exchange for access to a payout when you die.

This post will help you determine what life insurance coverage you need, using myself as an example. Your situation will be different than mine – no doubt – but this should give you a real-life family to compare to as you navigate the universe of insurance salesmen and products.

If you’re a (soon-to-be) parent of young children, and someone is recommending something wildly different than this, I’d pump the breaks to consider why.

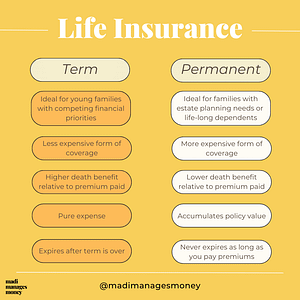

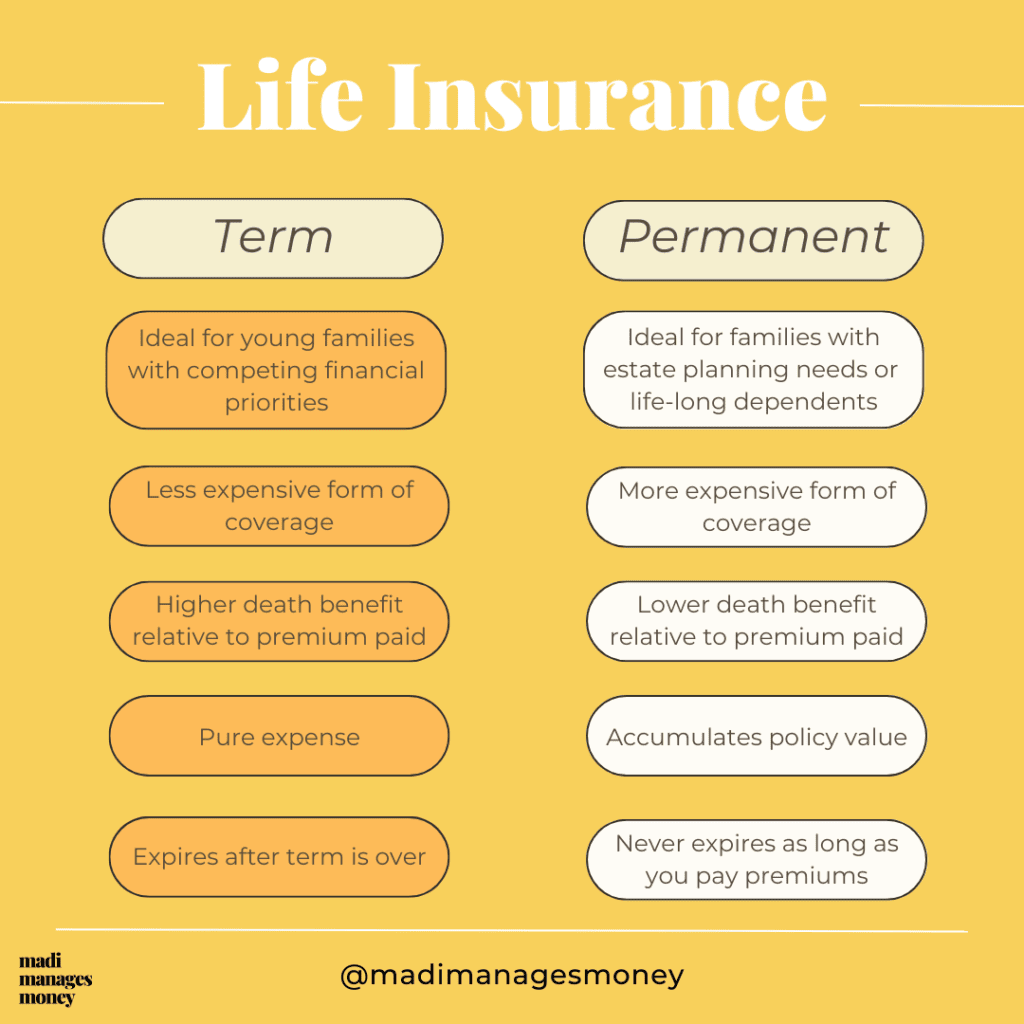

My term life insurance coverage

I have a $1 million term life insurance policy. To keep this coverage in place, I pay a fixed annual premium of $450. Over the 25-year life of the term, it will cost me a cumulative $11,250 to “rent” ongoing access to a $1 million potential payout.

It’s called “term” insurance because the policy is only in place for a specific period of time. If I outlive my 25-year term or cancel the policy, the premiums I’ve paid are purely an expense. I won’t get them back. I can cancel at any time by simply not paying the premium.

For more context on my costs, I’m 33 years old, married, and have a daughter who is almost two. My husband and I are considering having a second child, so we’re factoring double the expense (and utter chaos) into our needs. I’m also fairly healthy for my age and don’t smoke, which factor into my premium costs.

Both my husband and I earn incomes. He works full-time as a W2 employee, and I do contract work as a financial planner and sneak in freelance investment writing gigs when I can. If either one of us passed away, not only would we lose that person’s income, but it would also compromise the remaining spouse’s earning power. He has his own $1 million, 25-year term policy.

Calculating the $1 million death benefit

The payout of your policy is affectionately known as a “death benefit” in the insurance industry. To determine the right size death benefit, estimate your family’s expenses from now until your kids are financially independent. That’ll mean something different to every family, but here’s what we’re planning for.

We want to cover our children’s basics needs, plus most of their college undergraduate costs. In essence, we want to launch them into early adulthood with a manageable amount of student loan debt, at most.

Our breakout of rough estimates looks like this:

- Public university tuition in 18 years: $300,000 ($150,000 total x 2 kids)

- Daycare & childcare costs: $200,000 ($20,000/year x 5 years x 2 kids)

- Future mortgage if we buy a bigger house: $300,000

- Other living expenses: $200,000

As you can see, this isn’t an exact science, and I’m not running numbers out to the penny. I’ve also left a little living expense cushion in the “other” category for whatever else could come up along the way. Despite being a relatively frugal family in a low cost of living area (#YINZ), we racked up $1 million in future costs pretty quickly.

Other methods for calculating your death benefit exist, with one of them being purchasing a policy that replaces your income instead. Some experts recommend sizing it at 10-12x your annual earnings.

I don’t recommend the income approach in isolation, because there are ways it can lead you astray. For instance, if you live well below or above your means, the death benefit you calculate may be too high or too low.

Yet, it’s not a bad idea to use both methods in concert as a sensibility check. In my case, both approaches land in the same ballpark, which confirms I have my number about right.

Choosing the 25-year term

I want this policy to last until my children are out of the house and financially independent of us. To my husband and me, this means out of undergrad. The 25-year term will put my daughter at age 26 when it expires. Plus, if we’d have another child in the next two years, they’d be freshly graduated from college, too.

If I could go back and do one thing differently, I’d get the policy earlier in my life with a 30-year term. I’m healthy, so my premiums are still pretty low, but I didn’t take out this policy until I was 33, when my daughter was already here. If you’re not a parent yet but would like to be, getting term insurance ahead of time is a way to lock in the lowest premiums.

Why I chose term & not permanent life insurance

I opted for term insurance because of its low annual cost to keep a policy in place during the years I may need it. At a lower premium, I can maximize the amount my young family gets if I pass away, which is my primary objective. Generally, this makes term the right life insurance coverage for young families.

Permanent insurance, on the other hand, has substantially higher ongoing premiums. Getting the same $1 million death benefit would be cost-prohibitive.

As of April 2023, according to Nerdwallet, the average annual premium for a $500,000 whole life insurance policy for a 30-year-old woman is $4,015. For a 40-year-old woman, this jumps to $5,937. I pay $450 a year for $1 million in term insurance.

To access just half of the death benefit I have through my existing $1 million term policy, I’d be paying about 10x my current annual premium for a whole life policy. (Whole life insurance is the most common type of permanent insurance.)

Further, I really only need this policy in place for a finite amount of time. Because my husband and I have already achieved Coast-FI (which is the financial independence milestone you reach when you have enough saved for traditional retirement), we don’t anticipate needing coverage when our kids are grown. For this reason, having insurance for a specific term instead of our entire life makes the most sense.

My philosophy on life insurance coverage as a CFP

I don’t view insurance policies as an investment. Instead, insurance has a very specific purpose in my financial plan: to cover the financial loss of me not being there to provide for my family.

I’m not relying on it for growth or as a way to diversify my assets. There are plenty of more liquid, less expensive ways to do this in a regular old investment account for someone with my level of wealth.

Money is a limited resource with competing priorities in my family. I like knowing extra cash flow is there if I need it and not tied up in an insurer’s guaranteed account, earning a measly 1-3% a year.

I’ve taken out enough life insurance to cover all of my family’s future needs but not much more. With the annual “savings” I’m able to recapture by forgoing permanent insurance and opting for term (at least $4,000), I invest in low-cost, diversified index funds.

If history is any indicator, I’m likely to earn a nominal return (i.e. before inflation) of about 8% a year on my investment portfolio until I retire.

Related Post: Invest for Retirement or My Kid’s College Tuition? How to Do Both.

Other Life Insurance Coverage FAQ

Why is permanent insurance so expensive?

Permanent insurance is designed to stay in place your whole life, so the insurer prices in the fact that a payout is inevitable.

Whole life insurance (the most popular type of permanent insurance) also takes a portion of your premiums and stashes them in a cash value account for you. Your cash value account is nothing more than a bank account held at your insurer that guarantees a ~1-3% return. Said differently, permanent life insurance coverage is so expensive because the insurer’s forcing you to save your money. If you cancel your policy, you can usually get the cash value back.

Insurance sales agents lean on the cash value feature really hard in their pitch, because they know no one likes to fork over money you’ll never get back. “You’ll always get part of your money back, even if you cancel. Don’t throw away your premiums at term insurance!” Recognize this isn’t as big of a perk as it seems.

If the concept of getting cash value back appeals to you, then you should 💛 the idea of never giving that money to the insurer in the first place. Unless you need permanent insurance for a specific need (see the next FAQ), take out a term policy, pay a lower monthly premium, and shovel the savings into your own investment accounts.

When is permanent life insurance coverage appropriate?

You might consider permanent insurance coverage if you’re absolutely caked-up 🎂 or if you have a life-long dependent.

Permanent insurance can pass wealth to heirs outside of the probate process. This might be you if you’re a higher earner who relentlessly maxes out all of your other tax-advantaged accounts year after year. Life insurance policies grow tax-deferred, so this is like another form of tax-advantaged account.

It could also make sense if you expect to inherit substantial assets during your life, enough so that your estate is taxed at death. In 2023, a couple who’s married, filing jointly would need to have over $26 million in assets when they pass away to be subject to any federal estate taxes.

Permanent insurance policies provide your heirs with a liquid chunk of money to pay estate taxes. A girl can dream, but let’s acknowledge federal estate taxes are a much smaller problem than most people think. Only 0.07% of Americans who passed away in 2019 paid any estate taxes.

Permanent insurance can also make sense if you have a lifelong dependent. Ironically, I’ll only need life insurance during the years when I’m least likely to die, which is why my term policy is to cheap. The cost of a term policy that lasts your whole life would be much higher, because the insurer prices in the increasing odds that they’ll be paying your death benefit. At that point, locking in an annual premium for your whole life through permanent insurance might be the best choice.

Related Post: How the Rich Stay Rich: The Estate & Gift Tax Exemption

Do I need a life insurance policy in addition to coverage I have at work?

Probably, and if you have children, definitely.

Many companies offer group term life insurance as an employment benefit. You can access coverage equal to 1x your salary at little to no cost to you. Then, if you’d like to bump up your coverage, you can usually send a few extra bucks from your paycheck to access a death benefit of 2x your salary.

This is an awesome benefit – take full advantage of it – but group term life insurance alone won’t cut it if you have dependents. Let’s say you earn $100,000 a year and bump up coverage to 2x your salary, that leaves you with just $200,000 for your family if you pass. You witnessed earlier how quickly we stacked up $1 million in future costs for my family.

Group term insurance at work is also contingent on your continued employment. If you leave, you lose access to it and forgo the benefits of locking in your own supplemental term policy at a young age.

When I was in my twenties and didn’t have a child, relying on group term policies as my only form of life insurance is exactly what I did. Instead, I could have locked in an ultra-low term life insurance premium if I got a supplemental policy outside of work. Even if I switched jobs, I’d still have it in place.

Should nonearning spouses have life insurance?

Generally, yes. Although nonearning spouses aren’t necessarily generating revenue, they’re undoubtedly doing a boatload of unpaid labor that falls to someone else if they’d tragically pass away. In 2023, if a stay-at-home-spouse were paid for her contributions, she’d earn about $184,000. This estimated salary quantifies a cost you’d want to replace with insurance.

I joked about it before in this post on Spousal IRAs, but the earning spouse would suddenly have A LOT more to do than simply hire a nanny if their spouse passed away. In fact, it’s not uncommon for surviving spouses with children to downshift their own careers, and sometimes earnings, when a spouse passes. That could leave your family sputtering on a single, smaller income.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investments may be appropriate for you, consult with your financial advisor.