Target date funds make up approximately $3.3 of the $8.9 trillion assets in all defined contribution plans. As of 2019, 58% of all 401(k) participants owned one, up from just 19% in 2006. (Source: Morningstar)

It begs the question: Can something that’s available to everyone be any good?

This article outlines the pros, cons, and how to use target date funds. Your retirement might depend on it. 🙂

An Ideal Use Case: Young Investor, Small Balance

My first big-girl job was with a financial analyst development program for a bank.

Most of my coworkers were male but otherwise in the same stage of life as me. We’d just graduated from college and were the cringeworthy combination of bold and naive.

As Ruth Langmore from Ozark would say, we “didn’t know sh*t about f*ck.”

Nevertheless, I remember sitting in our bullpen (the glorified closet where they sat the rookie analysts), listening to my 22-year old male colleagues discuss their 401(k) investments with the knowingness of a tenured professor.

Most of them were trying their hand at building a custom portfolio to outpace the market.

Despite knowing just as much as they did about investing at the time, I remember listening quietly. A seed of doubt had been sowed.

I worried if the target date fund was good enough that I elected to plow my money into. The guys were clearly putting more effort into managing their accounts than me.

What was the catch?

What Are Target Date Funds?

Target date funds are a one-stop shop investment for retirement. They’re well-diversified portfolios that can be used as the sole holding in your account.

The idea is simple: you pick one that corresponds to your retirement year, and the investment manager handles the rest. It’s frictionless, like putting your account on autopilot.

Target date funds are usually “fund of funds.” By picking just one, you’re purchasing a mixture of several underlying portfolios.

Since Vanguard is the biggest player in the target date arena with a 36% market share, we’ll use them as an example.

When you invest in a Vanguard Target Date Fund, you’re buying a mixture of Vanguard index funds. That mixture is based on the number of years you have left until retirement and is determined by the target date fund manager.

If you’re a younger investor or have recently enrolled in a 401(k) at a new job, target date funds are appealing. You gain access to instant diversification without wasting time managing a small portfolio.

If you’re getting closer to retirement or have a larger account balance, pay special care to the target date fund you select. You’ll want to make sure that the fees are reasonable and that it aligns to your risk tolerance.

Target Date Funds Follow an Investment Glide Path

An investment glide path is what makes a target date fund, a target date fund. It refers to the gradual transition your fund makes from riskier holdings (like stocks) to more conservative ones (like bonds).

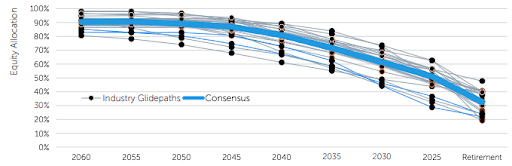

The graph below is the industry average investment glide path. It shows the percentage of equity (aka stocks) you’d expect to hold across a range of retirement years.

If you’re 30 and plan to retire when you’re 65, the 2060 consensus portfolio with 90% in stocks is most relevant to you.

Source: Newton Investment Management

As you can see, when you’re in your 20s and 30s, your target date fund goes hard in the stock market. The fund manager willingly accepts extra investment risk during these years to shoot their shot at higher returns.

Gradually, as the years pass, the manager reins in the investment risk. Divesting riskier holdings in favor of more stable ones creates that downward slope.👆

(For individual target date funds, this chart looks more like a staircase than a smooth slope.)

Once you reach the end of the investment glide path, a final, more conservative mixture is reached. This static allocation acts like a parking lot until retirees withdraw their money.

All the while, no buying or selling was required on your part; this was all conducted on your behalf by the target date fund.

Between now and the year you’re planning to retire, you could theoretically outsource all decision-making and rebalancing required in your account with a target date fund. For me, that removes a ton of friction and analysis paralysis.

Note, however, that you have no commitment to keep your money in a target date fund until retirement. They’re fully liquid, meaning you can buy and sell them at any time.

You can also split your money between multiple target date funds. Let’s say you plan to retire in 2057. You could put 50% of your money in the 2060 fund and 50% of your money in the 2055 fund.

How Much Do Target Date Funds Cost?

Because most target date investments are “fund of funds,” they have two layers of fees to consider.✌️

(Don’t let this scare you. As you’ll see, they can still be cost-effective.)

The first layer is the fee paid to the target date fund itself. This is the cost to manage your account according to the investment glide path.

It gets paid to a mutual fund or something called a collective investment trust (CIT).

All you really need to know about CITs is that they’re good news for you. Big companies use them to negotiate lower fees than what their employees could get through a mutual fund.

The second layer is the expense ratios of the underlying funds.

Continuing with our Vanguard example, fees would look like this:

- First layer – 0.08% fee paid to Vanguard Target Retirement 2060 for glide path management

- Second layer – 0.08% fee paid to underlying Vanguard index funds

All in, you’re looking at 0.16% paid in investment management expenses to completely automate your portfolio. Even on a $100,000 investment balance, that’s $160 per year.

Vanguard is among the industry’s lowest-cost providers, so this is admittedly a flattering example. Yet, the industry’s weighted average fee is 0.34%. That’s still only $340 per year paid in expenses on a $100,000 portfolio.

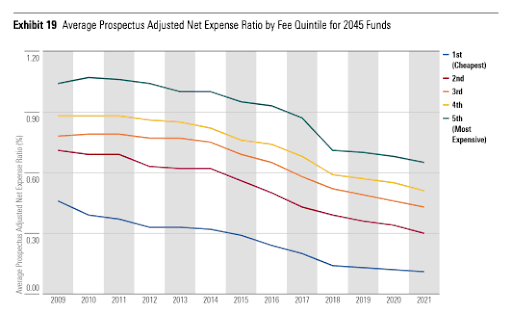

The graph below shows the average cost of target date mutual funds (not including CITs) broken into quintiles. The most expensive quintile is right around 0.70%.

It’s safe to assume that adding CIT data to this mix would pull the averages even lower.

Aside from the explicit cost of paying management fees, I’d also consider opportunity cost. Is managing your own account a good use of your time and energy?

Remember my colleagues who were jockeying to beat the market with their $9,000 account balances? Even if they went to the moon (which is highly unlikely – no offense, boys), their stellar returns would still only be on the basis of $9,000.

They’d have been better off focusing their time and effort on gaining valuable skills to grow their incomes than earning an extra 10% on their $9,000.

Moreover, target date funds are significantly cheaper than hiring a financial advisor to manage your money. They’d run you ~1% per year to more or less do that same thing with your portfolio.

- $100,000 * 1.00% = $1,000 annual fee with a traditional financial advisor

- $100,000 * 0.08% = $80 annual target date fund manager fee

Advisors are keen to criticize target date funds because they’re a viable alternative to hiring them for money management. I’d take their analysis with a grain of salt, especially if they’re implying they could earn better investment returns.

Where advisors shine is helping you make smart financial planning choices, like contributing to the right tax-advantaged accounts. (This can easily add up to thousands of extra dollars per year into your pocket!)

They can also confirm if your target date fund matches your overall investment risk tolerance, which is the single most important investment decision you make.

They won’t, however, be able to consistently outperform your target date fund, unless they’re taking more risk. Try as they might, there’s no secret investment sauce.

Related: Top 5 Reasons to Invest in Your 401(k)

The Pros of Target Date Funds

- Autopilot – If you suffer from analysis paralysis, target date funds might be your jam. Put all investment decisions for years to come on autopilot.

- Pick just one – Achieve instant diversification by investing in just one that matches the year you plan to retire.

- Cost-effective – Even with two layers of fees, target date funds are less expensive than hiring a financial advisor to manage your account. They’re also appealing compared to managing your own account. Your time is better spent growing your income, especially early in your career.

- No minimums – Target date funds in a defined contribution plan have no minimums. Gain access to professional management even on small balances.

- Not sacrificing returns – If you believe in low-cost diversified index investing, you’re a good fit for target date funds. That’s what most of them invest in, after all. The only return “sacrificed” is the cost of managing the investment glide path.

The Cons of Target Date Funds

- Two layers of fees – Target date funds are “fund of funds” and do have an extra layer of fees baked into them. On the more expensive end, you could pay ~0.70% in fees to the target date manager. This is more likely at smaller companies.

- Cookie-cutter – They’re one-size-fits-all. This can feel like a loss of control on your part.

- Investment glide path steps – In reality, investment glide paths look more like staircases than a smooth, downward slope. Each step down in risk to the next tread presents market timing risk. For instance, if you held a target date fund in 2022 that was scheduled to switch some of the portfolio over to bonds, your manager may have been forced to sell stocks into a depressed market.

- Not enough stock exposure early on – If you’re truly a young, aggressive investor, you should be investing solely in a portfolio of diversified equities early in your career. Some target date funds do offer this, but most start at 90% stocks and 10% bonds as their most aggressive portfolio. That 10% sliver can hold you back.

Related: Should You Be an Aggressive Investor?

The Verdict: Yes, Target Date Funds Are Good Enough 💯

Reflecting back on the scene at the beginning of this post, the younger, meeker version of myself should feel vindicated. Her investment selection was textbook.

The ideal use case for target date funds are young folks and investors with small balances, like when you start a job at a new company. I was both.

Target date funds could also work for someone who’s getting close to retirement or has a bigger account, but that’s a judgement best made on a case-by-case basis.

If you want to feel confident that your target date fund is good enough, take these two steps:

- Review the two layers of expenses. Compare them to the average fee charts in this article for reference. You can find info about your target date fund fees in your 401(k)’s Summary Plan Description. If fees are high, you’re comfortable managing your own money, and it’s worth your time to do so, I’d explore other investment choices in your 401(k).

- Ensure your risk tolerance matches your fund’s investment mix. Your target date fund will likely invest at least 90% in stocks if you’re not retiring for 30+ years. If the thought of your account falling by 10% (just making this number up as an example) sends you reeling, it might be too volatile for you to tolerate.

I’m a fan girl of target date funds. They remove barriers for regular folks (like us 🙋♀️) who otherwise might not invest. With them, you get cost-effective, professional management at no minimums.

There’s no catch, but they do require patience on your part. Pick one, sit back, and let the investment glide path do the heavy lifting for years to come.

Thanks for reading!

Madi

Resources:

- Morningstar: 2022 Target Date Strategy Landscape

- Newton Investment Management: The Power of the Consensus Glide Path

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investments may be appropriate for you, consult with your financial advisor.